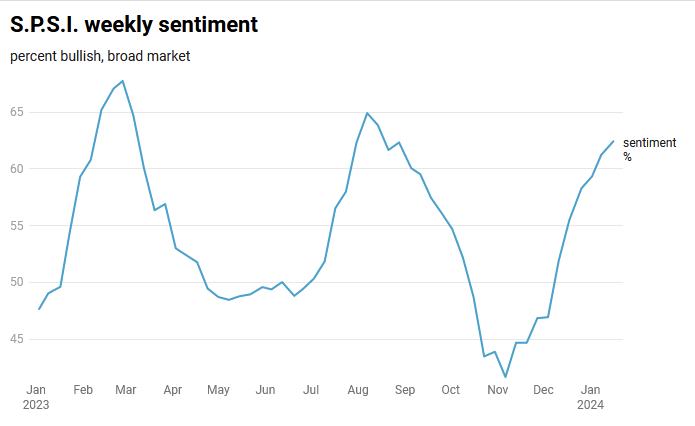

Weekly market sentiment is on the rise as the overall number reached 62.42 %, the highest since August of 2023 when it had topped the prior week at 64.9%. This is an increase from the week of January 8th 2024 reading of 61.22% and 59.34% the week before that.

The Financials sector topped the pack with a sentiment score of 81.93%, the highest of all sectors. This is followed by Technology, which achieved a score of 64.37%. Technology is the most advancing sector jumping from 61.54% the week of January 8th, 2024. The Utilities sector remains the most unappreciated asset, scoring steadily 22.73% again this week. Energy was second-to-last with 48.55% but declining from 50% the week before.

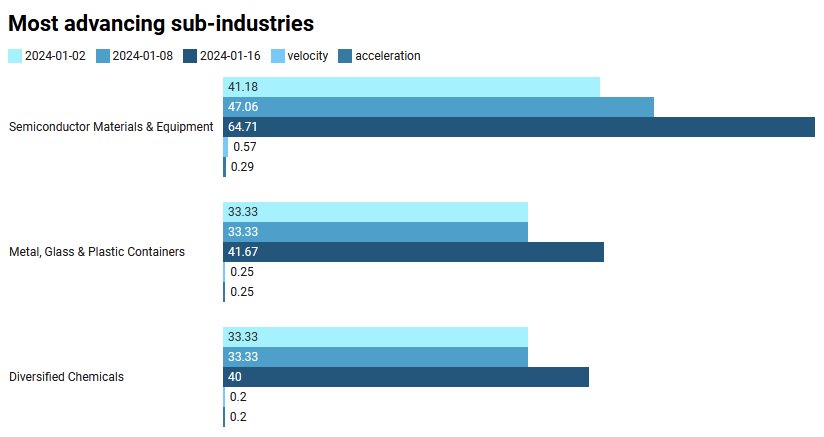

Let’s take a look at some of the sub industry moves.

Most advancing sub-industries for the week of 2024-01-15

In the sub-industry rankings, the Semiconductor Materials & Equipment has defied expectations and emerged as a steady grower, posting a remarkable sentiment score of 64.71%. This significant increase surpasses the previous weekly readings of 47.06% and 41.18%, demonstrating a remarkable surge in investor confidence. This unexpected development has surprised many analysts, as this sector has been traditionally viewed as a cyclical and volatile segment and already had made significant run in 2023. However, a combination of factors is driving demand for semiconductor equipment, including the continued growth of the semiconductor industry, chip makers’ expansion plans, and the increasing sophistication of semiconductor manufacturing processes. Investors seeking exposure to this dynamic sector may consider investing in companies that provide essential semiconductor materials and equipment.The momentum in the sub industry is rather powerful, achieving more than 50% increase from the previous week and showing no signs to stop. Trend followers may check companies like Applied Materials (AMAT), Terradyne (TER), KLA-Tencor Corporation (KLAC) and Lam Research Corp(LRCX).

Amidst a general surge in market sentiment, the Metal, Glass & Plastic Containers sub-industry has emerged as a standout performer, showcasing a steady acceleration and gaining significant momentum. With a sentiment score of 41.67%, this sector has surpassed its previous weekly readings of 33.33%. This unexpected development may take many analysts by surprise, as this sector has traditionally been viewed as a slow-growth segment. However, a confluence of factors is driving demand for metal, glass, and plastic containers, including the robust e-commerce industry, rising consumer disposable income, and the growing emphasis on sustainable packaging alternatives. Investors seeking exposure to this promising sector may consider venturing into companies that specialize in manufacturing these crucial packaging materials. Most notables companies in the sub industry are AptarGroup Inc (ATR) and Ball Corporation (BALL).

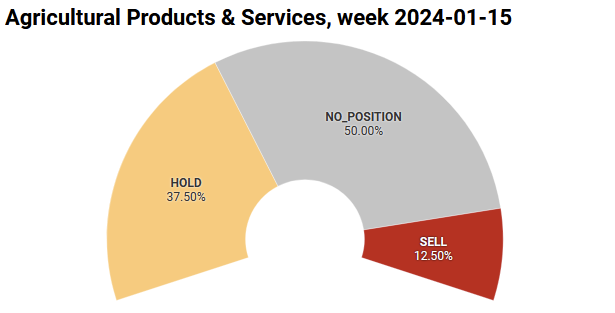

In stark contrast to the general market sentiment rally, the Agricultural Products & Services sub-industry has experienced a perplexing trend, registering a sentiment score of 37.5%, a notable decline from 43.75% the previous week.

This unexpected downturn has raised concerns among analysts, as the agricultural sector is often considered a resilient and stable segment, often weathering economic storms. However, a combination of factors is contributing to the sector’s recent struggles, including slowing inflation, lingering oversupply from previous years, and high inventory levels. While these challenges may seem daunting, investors with a contrarian mindset may see opportunities in this sector. As supply chain disruptions reoccurs and demand for agricultural products recovers, these companies could experience a rebound in their fortunes. Most notable players here are Archer-Daniels-Midland Company (ADM) and Bunge Limited (BG). Investors and traders considering a contrarian play in the area should carefully assess the risks and opportunities involved.

Current expectations remain towards inflation to slow in 2024, with the Federal Reserve likely to cut rates multiple times to support the economy. Low energy costs will also help to keep inflation in check. However, the labor market is expected to remain tight, which could put upward pressure on wages and price.

Overall, market sentiment remains positive, and the market is on track for another strong year. However, investors should be aware of the risks and make sure they are invested in a portfolio and risk corresponding to their goals.

The S.P.S.I. Tracker keeps you informed about top US equities and foreign markets. Our daily and weekly reports, backed by historical data, help traders and investors make better decisions for both short and long-term goals.